On Wednesday, the Federal Reserve announced it would begin tapering its asset purchases later this month.

But the Fed didn’t go all the way in reducing its easy money policies… as the central bankers opted not to raise interest rates from near zero.

While the news is hardly a surprise (the Fed telegraphed it well ahead of time)… the markets were happy to finally get confirmation on the timeframe… even happier that the planned reduction will be quite small… and ecstatic that zero rates would be remaining in place. The S&P 500 set a new all-time closing high on Wednesday.

The tapering process will see the Fed’s asset buying reduced by $15 billion per month (down from at least $120 billion per month) for November and December. The breakdown will be $10 billion less on Treasurys and $5 billion less on mortgage-backed securities (MBS).

If this pace stays, the Fed will be done with bond buying by the end of June 2022… But as of right now, it hasn’t committed to a set schedule—noting it would adjust its process along the way if necessary.

This month, it will buy an additional $70 billion of Treasury bonds… plus $35 billion of MBS. And in December, it will buy an additional $60 billion of Treasurys and $30 billion of MBS.

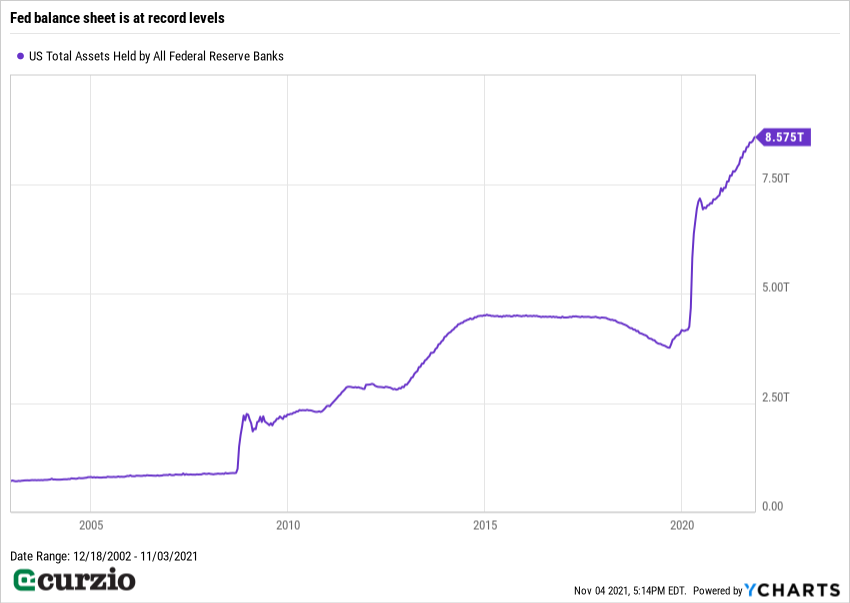

It’s important to note that the Fed already has an outsized balance sheet as a result of this increased buying since the COVID pandemic… a balance sheet that will keep growing for eight more months.

This means easy money is here to stay.

The Fed is taking it slow… and leaving lots of room to reverse course if needed. This “slow taper” is great for the markets.

But it’s not the main reason major indices jumped on Wednesday… That honor goes to the fact that there are still no rate hikes in sight.

Traditionally, stocks rally when the cost of money is low. And it can’t get any lower than zero.

While this is all good news for the markets… The Fed did get one thing wrong…

The Fed is making a mistake on inflation

For some reason, the Fed is still holding fast to its belief that current inflation is “transitory”… Jerome Powell and Co. seem to think all they need to do is to improve the economy… and inflation will miraculously disappear.

That simply isn’t true.

What the Fed doesn’t want to admit is that zero rates and extra bond buying all contribute to inflation…

It’s Economics 101: When too much money is chasing too few goods, prices rise. And zero interest rates plus ongoing bond buying equals more money in circulation.

Once inflation proves to be longer-lasting than the Fed is willing to say… the markets will be in trouble.

The longer we wait for the first rate hike in these conditions, the likelier we’ll need a sharper hike… and for longer.

This is how policy mistakes are made—by waiting too long to do something important… and, once the problem has grown too big to ignore… taking outsized steps to try to fix it.

History has shown that markets do well with moderate inflation… But high inflation—like we had in the 1970s—is bad for stocks… High interest rates are needed to stop prices from rising too high.

Already, stocks are showing signs of excess: Outsized daily volatility… abnormally high market price-to-earnings ratios… and historically low dividend yields are just a few such signs.

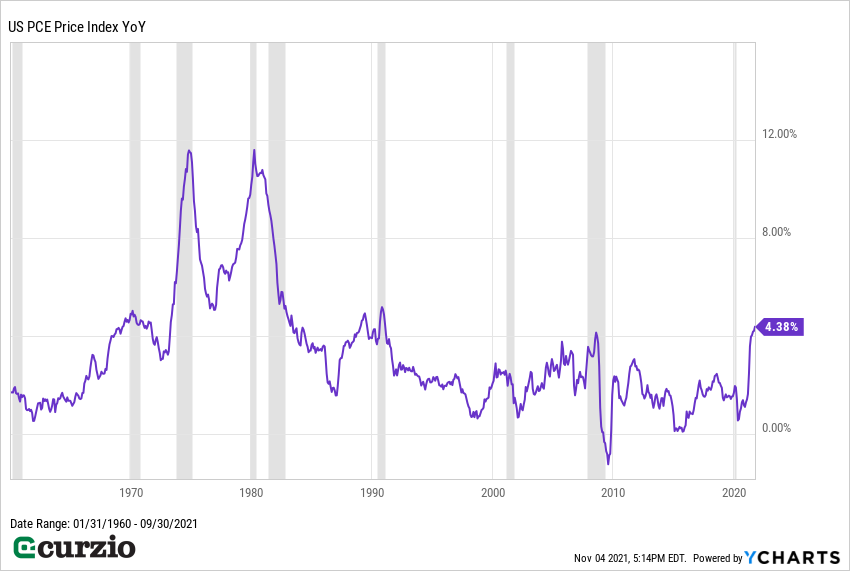

And PCE inflation—the Fed’s favorite metric—is at 4.4%… a level not seen since 1990.

The markets are shrugging off this fact—the allure of free money is just too great. And, judging from the market action, nobody really believes the Fed will ever take away the proverbial punchbowl.

And with year-end—a traditionally strong period for the markets—coming up, the chances of a meaningful pullback in the next few weeks are relatively low…

But not impossible.

Especially if inflation remains stubbornly high… and the Fed continues to ignore it.

The best course of action is to use some hedges to counteract the risk… and own high-quality stocks with steady dividends and significant pricing power. Those usually do well even with high inflation… and are easier to own during market pullbacks.

Editor’s note:

Take the guesswork out of hedging a risky market with Genia’s Moneyflow Trader strategy.

It’ll give you protection from the market’s downside… while still capitalizing on its upside.

It’s a strategy so powerful… Frank follows it with his own money.